Failed 1031 Exchange

Your Tax Options When the Deal Falls Apart

If you are reading this page, you may already be in a difficult spot. A 1031 exchange that was meant to defer your capital gains tax indefinitely has failed, and the gain you thought was protected is suddenly taxable. The replacement property fell through. The 45-day identification window closed. The 180-day deadline passed before closing. Or you simply could not find suitable replacement property in time.

Here is the good news. A failed 1031 exchange is painful, but it is rarely a complete loss. The right strategies, applied in time, can significantly reduce the tax bill and preserve more of your equity than you might think.

This page covers what triggers a failed exchange, when the tax actually becomes due, and what options remain open. The window to act is shorter than most investors realize, so the conversation should start as soon as you know the exchange will not complete.

What Counts as a Failed 1031 Exchange

A 1031 exchange can fail for several reasons. Each has different tax consequences and different remedies. The most common failure scenarios are:

You Could Not Identify Replacement Property Within 45 Days

The 45-day identification period is one of the most rigid rules in the tax code. From the date the relinquished property closes, you have 45 calendar days to identify potential replacement properties in writing to your Qualified Intermediary. Holidays, weekends, and extensions do not apply. If you do not identify within 45 days, the exchange fails.

You Could Not Close on Replacement Property Within 180 Days

Even if you identified replacement property within 45 days, you have only 180 calendar days from the sale of the relinquished property to close on the replacement. Financing delays, due diligence issues, seller backing out, title problems, and similar disruptions can push the closing past day 180. Once the deadline passes, the exchange fails.

The Replacement Property Was Worth Less Than the Relinquished Property

This is technically a partial failure rather than a complete one. The exchange itself is still valid, but the difference between the values (called boot) is taxable in the year of the exchange. Many investors are surprised to discover that “trading down” creates a taxable event even when the rest of the exchange completes successfully.

You Received Cash or Other Non-Like-Kind Property

If any of the proceeds came back to you in cash, or if you received non-like-kind property as part of the exchange, that portion creates taxable boot. The Qualified Intermediary rules exist specifically to prevent this, which is why the proceeds must flow through a QI rather than directly to the seller.

The Replacement Property Did Not Qualify

The replacement property must be held for investment or business use, not for personal use, resale, or as inventory. If you converted the replacement property to personal use too quickly, or if the IRS determines it was not held with investment intent, the exchange can be disqualified retroactively.

A Reverse Exchange Did Not Close Properly

Reverse exchanges (where the replacement property is acquired before the relinquished property is sold) have their own 180-day timeline and structural requirements. Failure of either side of the transaction can cause the exchange to collapse.

When the Tax Actually Becomes Due

This is the part most investors misunderstand. A failed exchange does not necessarily mean the tax is due immediately. The timing of when the gain becomes recognized depends on how and when the failure occurred:

If the Exchange Fails Within the Same Tax Year

If your relinquished property sold in Year 1 and the exchange fails within Year 1 (for example, you could not identify replacement property within 45 days and that 45-day window closed before December 31), the gain is taxable in Year 1. You report it on your Year 1 return.

If the Exchange Fails Across Tax Years (The Installment Sale Treatment)

This is the most important rule to understand. If your relinquished property sold in Year 1 but the exchange fails in Year 2 (for example, the 180-day deadline expired in Year 2), the IRS treats the failed exchange as an installment sale under IRC Section 453. The gain becomes taxable in Year 2, not Year 1.

This rule exists because the QI was holding your proceeds during the exchange period. Even though the cash technically came from a Year 1 sale, you did not have access to it until the exchange officially failed in Year 2. The IRS allows you to recognize the gain in the year the cash actually became available.

For investors whose exchange fails in early Year 2, this creates a critical planning window. You may have most of Year 2 to implement strategies that offset the gain before it lands on your return.

If You Receive Boot in a Partial Exchange

Boot is taxable in the year of the exchange itself, regardless of whether the rest of the exchange succeeds. If you closed your relinquished property in November and the resulting exchange included $200,000 of taxable boot, that boot is reported on your tax return for the year of the original sale.

Depreciation Recapture

Depreciation recapture is owed when the failed exchange creates a taxable event, just like in any other taxable sale. Recapture is calculated separately from the capital gain and is taxed at a maximum federal rate of 25 percent. For more on managing recapture, see our page on depreciation recapture strategies.

What Strategies Are Still Available After an Exchange Fails

The options available after a failed exchange depend on the timing of the failure and the size of the gain. Here is what typically remains on the table:

Installment Sale Election

If the exchange fails across tax years and the IRS treats it as an installment sale, you may be able to recognize the gain over multiple payment years rather than all at once. This applies when the failed exchange is structured in a way that allows installment treatment, which is usually the case when the QI was holding proceeds across the year-end. Working with your CPA on the Form 6252 reporting is essential.

Strategic Loss Recognition

If you have other investments showing losses (whether real estate, marketable securities, or business interests), recognizing those losses in the same tax year as the failed exchange can offset the capital gain. The losses do not have to be from real estate to offset real estate gains, as long as they are capital in nature.

Bonus Depreciation and Section 179 Offsets

If you have business activity or own depreciable assets, accelerated depreciation deductions taken in the same year as the failed exchange can offset the gain. This is particularly effective when the gain creates a high-income year that benefits from large depreciation deductions. See our pages on bonus depreciation strategies and Section 179 deductions.

Charitable Giving in the Same Year

Coordinated charitable contributions in the year of the failed exchange can reduce taxable income substantially, particularly when structured to maximize deduction value. Donor-advised funds, charitable remainder trusts, and other structured giving vehicles all become more powerful in a high-income year. See charitable giving tax strategies for the broader toolkit.

Opportunity Zone Investment

You have 180 days from the recognition of the capital gain (not from the original sale) to reinvest the gain into a Qualified Opportunity Fund. This means even after a failed exchange, you may have time to defer the gain again by routing it into a QOF investment. The same caveats apply as in any other QOZ investment, including the 10-year hold horizon and the end of the deferral period in 2026 under current law.

Advanced Tax Mitigation Strategies

When the basic offsets above are not sufficient to cover the gain, advanced tax mitigation strategies become relevant. These include structured loss programs, accelerated depreciation against business income, and timing strategies that smooth tax exposure across years. The right combination depends on your full tax picture and the size of the gain.

To see whether advanced strategies fit your situation, review our page on who qualifies for advanced tax mitigation.

Mistakes to Avoid After a Failed Exchange

A failed 1031 exchange is stressful, and the wrong reaction can make the tax situation worse. The most common mistakes we see:

- Waiting until tax filing season to address it. Most offset strategies need to be implemented before December 31 of the year the gain is recognized. By the time you sit down with your CPA in March, your options are dramatically narrower.

- Assuming all the proceeds are immediately taxable. Depending on when the exchange failed, you may have installment sale treatment available, which can spread the gain across multiple payment years.

- Trying to fix the failure after the fact. Once the 45-day or 180-day window closes, no amount of paperwork or rebooking can resurrect the exchange. The IRS does not grant extensions for missed deadlines except in narrow disaster-related situations.

- Forgetting about depreciation recapture. Many investors plan for capital gains tax but forget that recapture is taxed at a higher rate and cannot be fully offset by every strategy.

- Ignoring state tax exposure. Federal planning is only half the picture. For investors in California, New York, Oregon, Hawaii, or other high-tax states, state tax planning needs to be part of any post-failure strategy.

- Working with a CPA who has never handled this before. Failed exchange treatment, particularly the installment sale election, has procedural requirements that need to be handled correctly on the return. Make sure your CPA has experience with the specific situation, or coordinate with one who does.

How Time-Sensitive Is This?

Very. The window to apply offset strategies closes at the end of the tax year in which the gain is recognized. For most failed exchanges, that means strategies need to be in place before December 31.

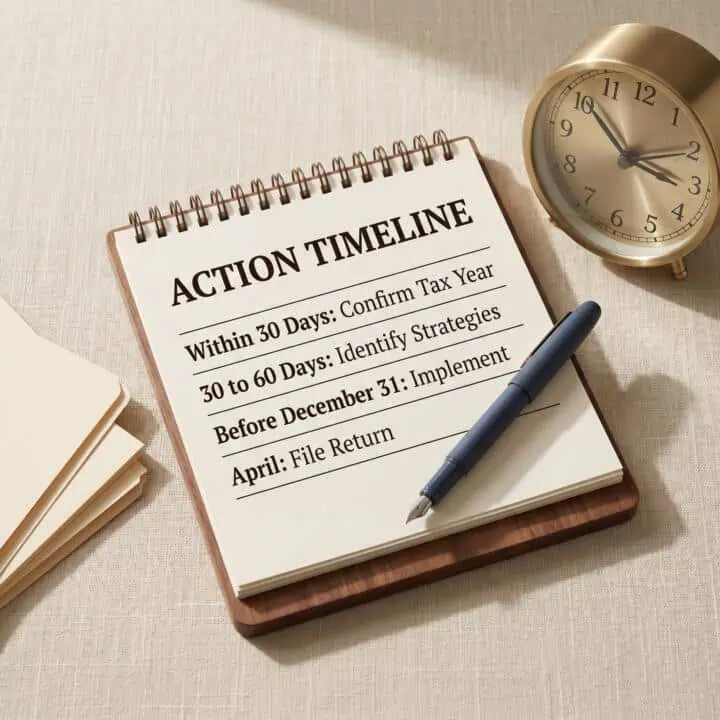

A practical timeline:

- Within 30 days of the failure. Confirm with your CPA which tax year the gain will land in. Understand exactly how much tax is owed and what type (capital gain, depreciation recapture, state).

- 30 to 60 days after. Identify which offset strategies fit your situation. The right combination depends on your overall income, your other investments, and your ability to participate in advanced planning.

- Before December 31 of the recognition year. Most offset strategies must be implemented and documented before year-end. This includes bonus depreciation purchases, charitable contributions, QOZ investments, and structured loss programs.

- April of the following year. File the return with the gain properly reported and the offsets properly documented.

If your exchange has already failed, the most important thing is to start the conversation now, not after the holidays.

Frequently Asked Questions About Failed 1031 Exchanges

Can I extend the 45-day or 180-day deadline?

In almost all cases, no. The IRS has only granted extensions in narrow situations, primarily federally declared disasters where the IRS specifically issued relief notices. Personal hardship, financing difficulties, market conditions, or seller issues do not justify extensions.

If I missed the 45-day deadline, is there any way to still complete an exchange?

Not for that transaction. The 45-day identification window is absolute. However, if you have not yet sold the relinquished property, you can restructure your plans and pursue an exchange on a different timeline. The deadline only applies once the relinquished property has actually sold.

My QI is still holding my proceeds. Am I still in the exchange?

Maybe, depending on the timing. If your 45-day window has closed without identification, or your 180-day window has closed without acquisition, the QI is generally required to return your proceeds after the relevant period ends. The exchange has technically failed at that point, and the proceeds become taxable.

Can I do a partial exchange instead of a full failure?

Yes. If you identified replacement property within 45 days and closed on it within 180 days, but the replacement property’s value was less than the relinquished property’s value, the exchange completes as a partial exchange. The difference (boot) is taxable, but the rest of the gain remains deferred. This is often a better outcome than letting the entire exchange fail.

Does a failed exchange affect my ability to do another 1031 in the future?

No. A failed 1031 exchange does not restrict future exchanges. As long as the next transaction meets all the 1031 requirements (held for investment, like-kind property, proper QI structure, 45 and 180-day timelines), it can qualify for full deferral.

What about a failed reverse exchange?

Reverse exchanges have similar 180-day timelines and structural requirements, with their own failure modes. The tax treatment of a failed reverse exchange depends on which side of the transaction failed and when. The same general principles apply: the gain becomes recognized when the exchange officially fails, and the offset strategies described on this page remain available.

Is it worth the effort to offset the gain rather than just paying the tax?

This depends entirely on the size of the gain and your overall tax picture. For a $50,000 gain, the cost of implementing complex offset strategies may exceed the tax savings. For a $500,000 gain, the math typically supports significant planning effort. A 15 to 30 minute conversation can usually clarify whether offset strategies are worth pursuing in your specific situation.

Get Ahead of the Tax Bill

A failed 1031 exchange is one of the few tax situations where the difference between acting quickly and waiting is measured in tens of thousands of dollars, sometimes more. The offset strategies that work best all require implementation before year-end, and the documentation requirements take time to put together properly.

If your exchange has failed, or you can see that it is going to fail, do not wait:

- Contact our team immediately to discuss your specific situation

- Read our tax mitigation overview for the broader toolkit

- See who qualifies for advanced tax mitigation to understand whether the larger strategies fit your situation

- Review capital gains tax strategies for real estate investors for the full picture of what may apply

We have helped investors recover from failed exchanges for nearly three decades. There are almost always options, but the longer you wait, the fewer remain.